Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

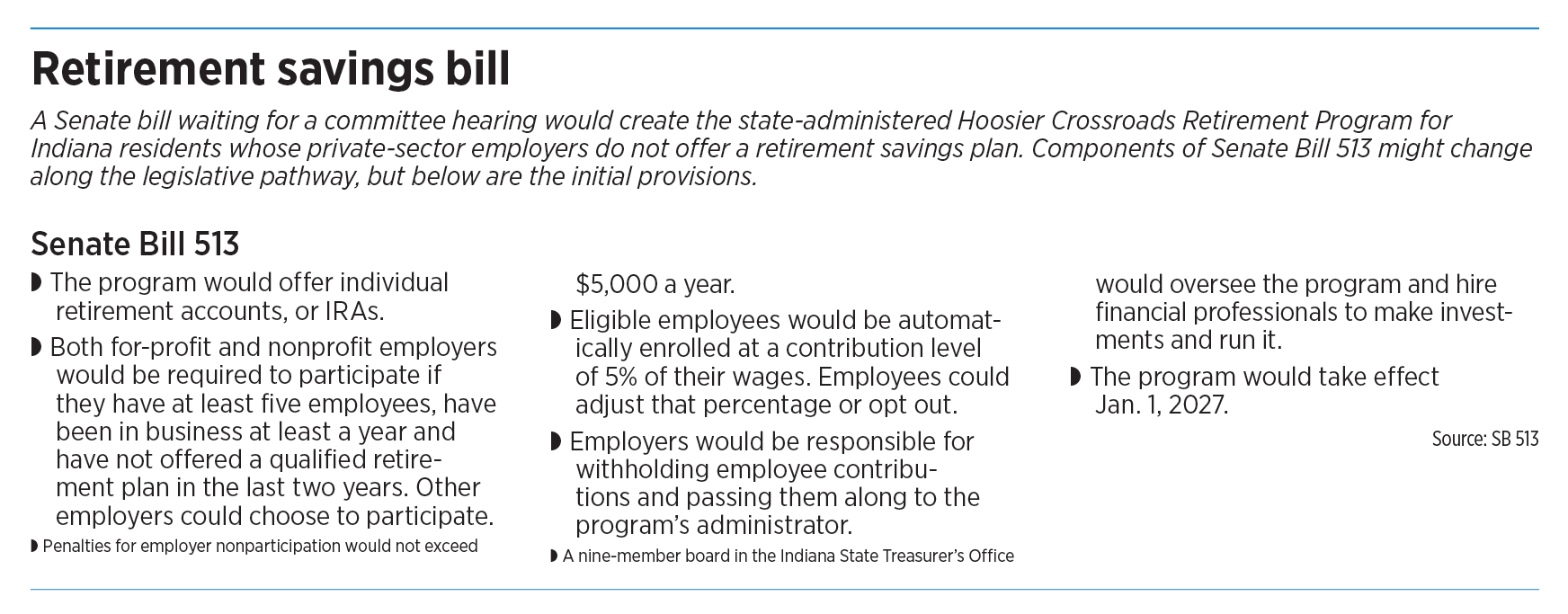

Indiana could soon join the growing number of states that offer retirement programs aimed at private-sector employees.

Over the last decade, 20 states have passed legislation enabling the creation of state-facilitated retirement savings programs—and Indiana is one of four states considering similar legislation this year.

The big-picture goal: provide an additional retirement savings option for private-sector workers whose employers do not offer such plans.

Details of the programs, sometimes called state-sponsored or state-administered plans, vary from state to state. But in general, the programs allow employees to set up retirement accounts—typically, an individual retirement account, or IRA—and direct a percentage of their paycheck into that account. Employers act as a pass-through, collecting those contributions and sending them to the program’s administrator.

“It just makes saving easier,” said Sen. Vaneta Becker, R-Evansville, who is one of three authors of Senate Bill 513. The other two authors are Sen. Greg Walker, R-Columbus; and Ron Alting, R-Lafayette.

SB 513 has been assigned to the Senate Appropriations Committee, although as of Tuesday, it had not been scheduled for a hearing—a key step in the legislative process.

The legislation faces pushback from at least one business group, but within the Statehouse, it has bipartisan support. So far, eight senators—six Democrats and two Republicans—have signed on as co-authors.

As introduced, the bill applies to for-profit and nonprofit employers who have at least five employees, have been in business at least a year and have not offered a qualified retirement plan in the last two years.

Eligible employees would be automatically enrolled at a contribution level of 5% of their wages, although employees could choose to adjust that percentage or opt out altogether.

Employers would be required to participate by withholding employee contributions and passing them along to the program’s administrator, and employers would face financial penalties of up to $5,000 per year for nonparticipation.

The program would be created and overseen by a nine-member board in the Indiana State Treasurer’s Office, and the board would hire outside financial professionals to make investments and run day-to-day operations.

The big picture

Employer-sponsored retirement savings programs such as 401(k) plans are a common way individuals can save for retirement. A significant percentage of employers do not offer such plans, though various sources offer differing figures on what that percentage is.

According to the U.S. Bureau of Labor Statistics, 30% of private-sector workers do not have access to a defined-contribution retirement plan through their employer.

Citing a 2022 fact sheet from the AARP Public Policy Institute, the nonpartisan organization Pew Charitable Trusts says 43% of Indiana’s private-sector workers, or just over 1.1 million people, lack such access.

And those without adequate retirement savings, Pew Charitable Trusts said, are more likely to need social assistance programs, placing a burden on state and national budgets. In Indiana, Pew said, that burden would cost the state nearly $6.9 billion in additional spending through 2040 if current retirement savings shortfalls do not change. Pew is advocating for state-facilitated retirement savings plans as a solution to the problem.

The argument makes sense to Becker, the bill’s author.

“I’m just hoping that we can [pass the legislation] this year, because if we don’t, we’re going to be penny-wise and pound-foolish in the future.”

One of the bill’s co-authors, Sen. Fady Qaddoura, D-Indianapolis, offered a similar view. “This is an important piece of legislation, and it is a proactive approach that would save the state money in the long term.”

Though employees can, of course, save for retirement on their own—perhaps by opening an IRA through a financial institution—people are 15 times more likely to save if they can access a retirement savings plan through their employer, said Angela Antonelli, executive director of the Center for Retirement Initiatives at Georgetown University.

“Too many Americans today are not saving enough for retirement,” Antonelli said.

Illinois and Oregon were the first states to establish state-facilitated retirement programs. Both passed the enabling legislation in 2015. Oregon began rolling out the program in 2017, and Illinois did so in 2018.

To date, 13 states have their programs up and running while seven others are working to do so. Indiana, Alaska, Mississippi and Tennessee are all either considering legislation or studying the issue in committee, according to the Center for Retirement Initiatives.

Though Democrat-heavy states were the first to establish such programs, Antonelli said, the success seen by those early adopters persuded other states—including Republican-led states—to pass similar legislation.

At the end of last year, she said, individuals had saved nearly $1.9 billion cumulatively in nearly 1 million retirement accounts associated with state-facilitated programs.

“That potentially means that there’s a million workers saving for retirement now that just a few years ago might not have been saving for retirement,” Antonelli said.

The opposition

Not everyone is supportive of SB 513, though.

“We really feel like this is a clear example of legislative overreach,” said Natalie Robinson, the Indiana director of the National Federation of Independent Business.

NFIB membership is open to independent businesses of any size, Robinson said, but more than half of the organization’s members have 20 or fewer employees. NFIB has about 11,000 members in Indiana.

Robinson said requiring employers to participate in a state-administered program would impose financial and administrative burdens on NFIB members. “It really is a drain on their already limited resources.”

The NFIB also maintains that such programs are unnecessary, Robinson said, pointing out that employees already can open and fund their own IRAs.

And, she said, in states that have adopted such programs, a significant percentage of employees choose to opt out.

According to the Illinois State Treasurer’s Office, which oversees the Illinois Secure Choice Retirement Savings Program, the program’s opt-out rate in December was 38%. The program also had just more than 156,000 participants who have saved more than $224 million cumulatively to date.

The Illinois program rolled out in 2018 for employers with 500 or more employees. Its final wave of rollouts was in November 2023 for employers with five to 15 employees.

The Oregon State Treasury, which oversees the OregonSaves program, said in its December 2024 report that participants had saved just more than $329 million combined in 133,000 retirement accounts. That program’s opt-out rate is 27%.

Oregon’s program rolled out from late 2017 to last July, beginning with the state’s largest employers first.

Robinson said she plans to testify against SB 513 when it is heard in committee.

The Indiana Chamber of Commerce has not taken a position on the bill, said Matt Ottinger, the organization’s director of digital media and legislative communications.

Qaddoura said he wants to hear the business community’s feedback on SB 513, and he fully expects the bill’s language to evolve as it makes its way through the legislative process.

“I’m approaching this with an open mind and an open heart,” Qaddoura said. “Our goal is not to push through legislation that is not meaningful.”•

Please enable JavaScript to view this content.