Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe NowThe competition among banks for deposits is strong right now—and that can translate into cash offers of up to several hundred dollars to customers who open new accounts.

Cash offers are not a new phenomenon, but they are a tool that banks and credit unions can use as needed to bring in new deposits—deposits that banks can then use to make loans. And it’s a tool that’s in widespread use locally now, with at least 10 banks and credit unions offering such incentives.

After a lull during the pandemic—and especially since interest rates started rising over the past two years—cash offers have picked up steam.

“It seems to be in full force again,” said Scott Ransburg, the Indiana market president of Columbus, Ohio-based Huntington National Bank.

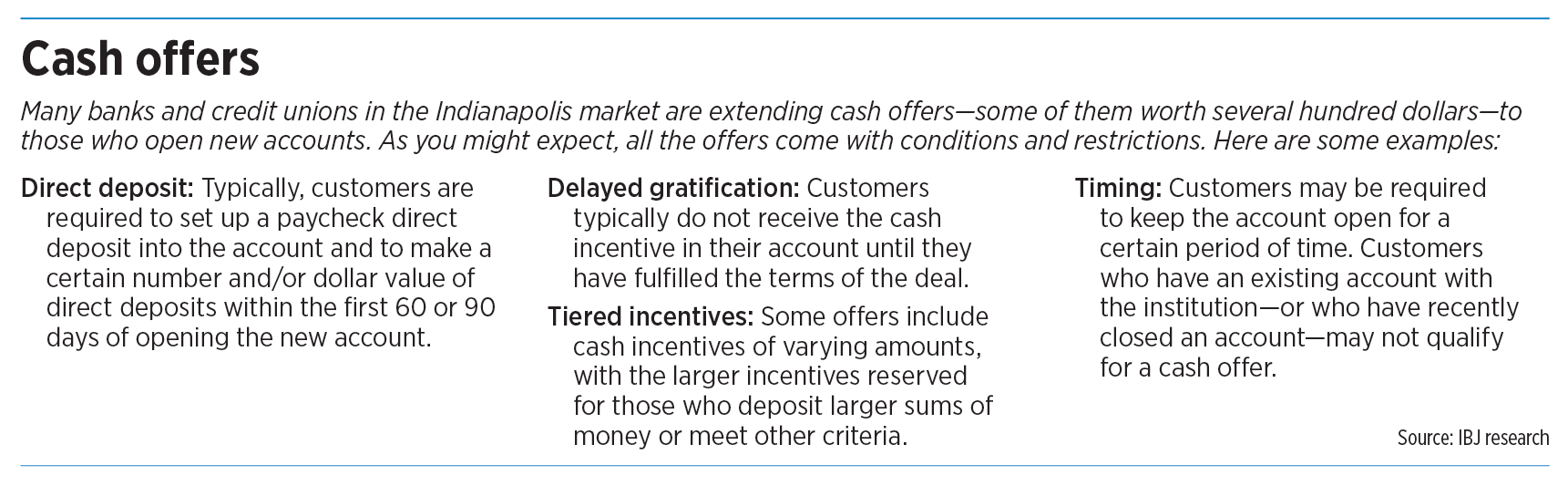

Huntington is offering incentives of up to $600 for individuals who open a new checking account if they deposit at least $25,000 into the account and keep the account open for at least 90 days. The bank is also offering smaller incentives of $200 and $400, which carry smaller deposit requirements.

Huntington has doubled its top incentive since December 2022, when the bank’s top offer was $300, according to previous versions of the bank’s website accessed via the Wayback Machine internet archive.

Credit unions are also using the incentive. South Bend-based Everwise Credit Union, whose operating footprint includes 19 Indianapolis-area locations, is offering $200 in cash to those who open a new checking account and meet certain requirements.

“Over the last two years, we’ve offered cash incentives more regularly to encourage people to switch their banking to Everwise,” Chief Marketing and Growth Officer Angie Dvorak told IBJ via email. “These offers were initially tied to special events, but as the big-box banks have blanketed our market with cash incentives, we’ve introduced our own offers to remain competitive.”

Those familiar with the banking industry say a variety of factors, from declines in deposits to interest rates and competitive factors, are all driving banks’ eagerness to extend cash offers.

During the pandemic, banks saw their deposits soar to record highs because customers shifted their spending and savings patterns while loan growth softened. The glut of deposits meant banks weren’t looking to attract new depositors.

According to data from the Federal Reserve, in 2020, bank deposits nationally rose 20.8% over the previous year—the highest one-year increase in history. Deposit growth slowed after that, and in 2023, deposits declined 2.7% from the previous year.

Curinos, a New York City-based firm that advises financial institutions, projects that the change in deposits this year will range from a 2% decline to 4% growth, said Olivia Lui, the firm’s senior vice president of channels advisory. Curinos expects growth of between 1% and 6% in 2025.

Another factor in the incentive deals is that as interest rates have risen within the past two years, banks have had to sweeten their offers to customers looking for better returns.

“Banks have seen the wave of people abandoning traditional savings accounts for high-yield savings accounts in recent years, and they’ve ramped up one-time cash incentives to slow that down,” Depositaccounts.com Chief Credit Analyst Matt Schulz told IBJ via email. (Depositaccounts.com is affiliated with the North Carolina-based online lending marketplace LendingTree Inc.)

Lui said the rise in online-only financial institutions is also putting pressure on traditional banks. Online-only institutions don’t have the expense of maintaining a physical network of branches, which allows them to offer higher interest rates than traditional banks.

That increased competition among financial institutions combined with sluggish deposit growth “creates kind of a zero-sum game,” Lui said.

The cash offers are often tied to checking accounts. “Most banks, it feels like, are trying to get that core operating account right now,” said John Jordan, the head of retail banking at Birmingham, Alabama-based Regions Bank.

Regions, which has 15 branches in Indianapolis and others around central Indiana, is currently offering a $300 cash incentive for new checking customers who meet certain conditions, which include linking the new account with a direct deposit and making at least $1,000 in direct deposits into the account within the first 90 days.

Jordan and others said checking accounts are important because consumers need them to conduct basic transactions like depositing their paychecks and paying bills. And once a bank wins a checking customer, the bank can then hope to win more business from that customer over time—maybe a mortgage, car loan or a credit card.

“Capturing that checking account is really important, just because then as customers grow, they usually will do their mortgage where they have their checking account and so on,” Ransburg said.

Brent Tischler, Old National Bank’s Milwaukee, Wisconsin-based CEO of Community Banking, offered a similar view. “Checking accounts are really the platform to grow deeper relationships over time,” Tischler told IBJ via email.

Evansville-based Old National operates 19 branches in the Indianapolis area. The bank is currently extending cash offers of $250 and $450 for new checking customers who meet certain criteria.

Looking ahead, Tischler said the interest rate environment and the competitive landscape will dictate how long Old National continues its cash offers.

Schulz, at Depositaccounts.com, said that if interest rates decline sharply, banks could scale back and offer bonuses to a “smaller, more select group of people” than is currently the case.

But Schulz doesn’t see cash offers disappearing any time soon.

“They’re too valuable of a tool for banks to attract new customers,” he said. “They know that with the right customer, they’ll make way, way, way more than that $200 or $300 on that customer over the years, so it makes sense for those offers to stick around.”

Ransburg said he thinks of cash offers as the “cherry on top” that can persuade customers to choose Huntington Bank over a competitor. “This catches people’s eye,” he said.•

Please enable JavaScript to view this content.