Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

Financial technology enables individuals to do everything from stock trading to retirement planning without ever talking to a financial adviser.

So it might surprise you to learn that the industry is in expansion mode, with job growth expected to significantly outpace overall U.S. job growth over the next several years.

Industry insiders cite several reasons for the growing demand for financial advisers: demographics, consumer preferences and the rise of so-called robo-advisers—the digital financial tools that can serve as a gateway to working with a human adviser.

“Twenty years ago, or whenever digital advisers were starting, there was a lot of concern that advisers would be replaced by these digital platforms,” said Karen Barr, CEO of the Washington, D.C.-based Investment Adviser Association. “And in fact, the opposite has occurred. It’s just exposed more potential clients to the industry and the value of advice. And many folks don’t want to work with just the algorithm. They want to work with humans.”

Danielle Ambrose, chief growth officer at Carmel-based Valeo Financial Advisors, said her firm is seeing growth in demand for its services. Valeo has about 125 financial advisers and expects to bring on 20 more this year.

“There’s a much larger need for investment advice,” Ambrose said. “Over the last few years, it has been much more competitive to attract and retain advisers.”

National projections also suggest a growing demand for financial advisers.

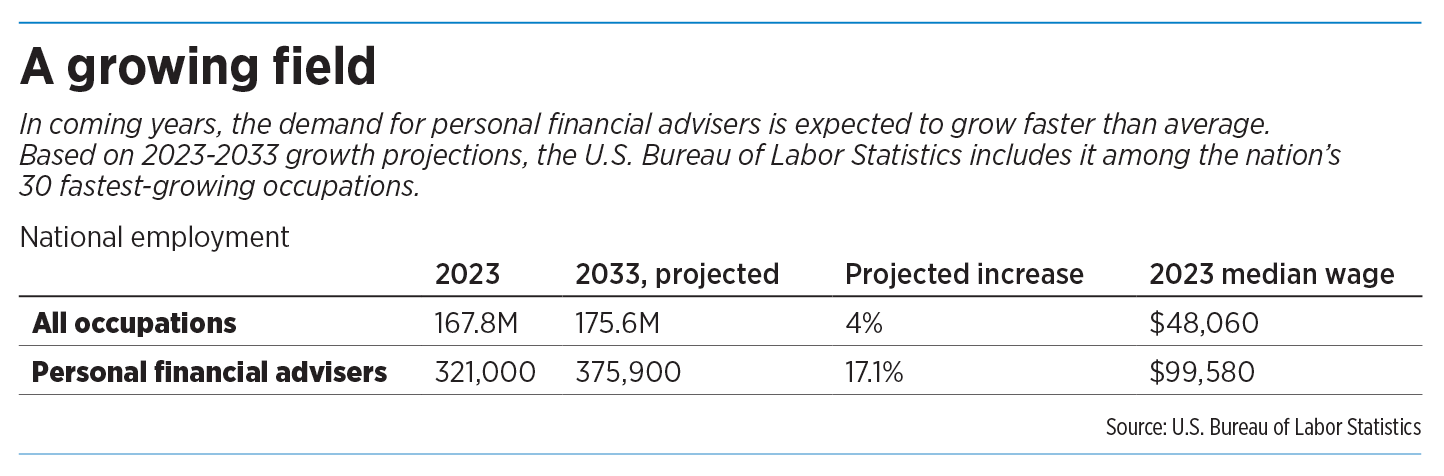

The U.S. Bureau of Labor Statistics lists personal financial advisers as one of the country’s 30 fastest-growing occupations, with projected employment growth of 17.1% from 2023 to 2033. That growth would represent an increase of almost 55,000 advisers, from 321,000 in 2023 to a projected 375,900 in 2033. (In comparison, the BLS projects that overall job growth for all occupations will increase 4% during this period.)

And Charles Schwab & Co. Inc.’s 2024 Registered Investment Adviser Benchmarking Study offers a similar outlook, though its numbers are slightly different.

The Schwab study predicts that the RIA industry will need to add 70,000 advisers over the next five years to keep pace with demand—and that’s on top of the openings that will be created by retirements and attrition.

In the financial world, the term registered investment adviser, or RIA, refers to a firm that acts as a fiduciary and is legally required to act in a client’s best financial interests. Such firms typically earn revenue by charging fees for their services. (Sometimes, the term RIA is also used to refer to the individual advisers who work for RIA firms.)

RIAs differ from broker-dealers, which are firms that typically earn revenue from commissions on the investment products they sell. Broker-dealers are duty-bound to sell only investments suitable for a client’s risk tolerance, financial goals and other factors—a different standard from the fiduciary standard RIAs must follow.

Both the Schwab study and the organization Barr leads are focused on RIAs.

Some of the demand for financial advice is driven by demographics, Ambrose said—the aging of the U.S. population creates a larger pool of people seeking retirement-related financial guidance.

Another factor, she said, is that digital tools such as online stock trading platforms have made financial transactions more accessible than ever before. And once people begin using something like an online trading platform, they might start thinking about their overall financial situation and decide to seek advice from a real-world financial professional.

Another factor driving industry growth, insiders say, is the desire for customized financial advice—especially among younger clients and those with considerable wealth.

“People don’t want cookie-cutter solutions,” said Jack Boudreau, co-founder and CEO of Indianapolis-based fintech startup Habits Inc.

Habits offers an online marketplace that helps individuals connect with financial advisers that fit their needs, including financial situation and goals. The platform is geared toward individuals in their 20s through mid 40s.

“Anyone below the age of 45, every aspect of their life in some way, shape or form has been somewhat customized by technology,” Boudreau said. “And that is what’s going to be very, very important for the future.”

Boudreau said the desire for customization also reflects financial industry trends in general. Until about 2020, he said, the industry was focused on helping people save for and plan for retirement. But over the past several years, consumers have become more apt to seek professional financial guidance for a variety of other life events. Those events could include buying a house, taking a new job or deciding what to do with a significant bonus payment—all situations that require custom advice.

“I believe … that the future of the financial adviser is really to be like a household’s chief financial officer,” Boudreau said.

Affluent consumers also seek personalized advice, in part because people who have more wealth also tend to have complex financial lives, said Chris Cotterill, president of Carmel-based Goelzer Investment Management.

Goelzer specializes in wealthy and ultra-wealthy clients. About half of the firm’s clients are families and individuals, and the other half are institutional clients such as foundations and endowments.

“Our clients are the type of clients that want a trusted adviser,” Cotterill said. “Our clients are not day traders.”•

Please enable JavaScript to view this content.